THE LITTLEST HOBO: IS BEING A TAX NOMAD A LUCRATIVE STRATEGY, OR AN EXPENSIVE MISTAKE?

Read more

March 3, 2026 | 12 min read

Author: Andy Wood

INTRODUCTION

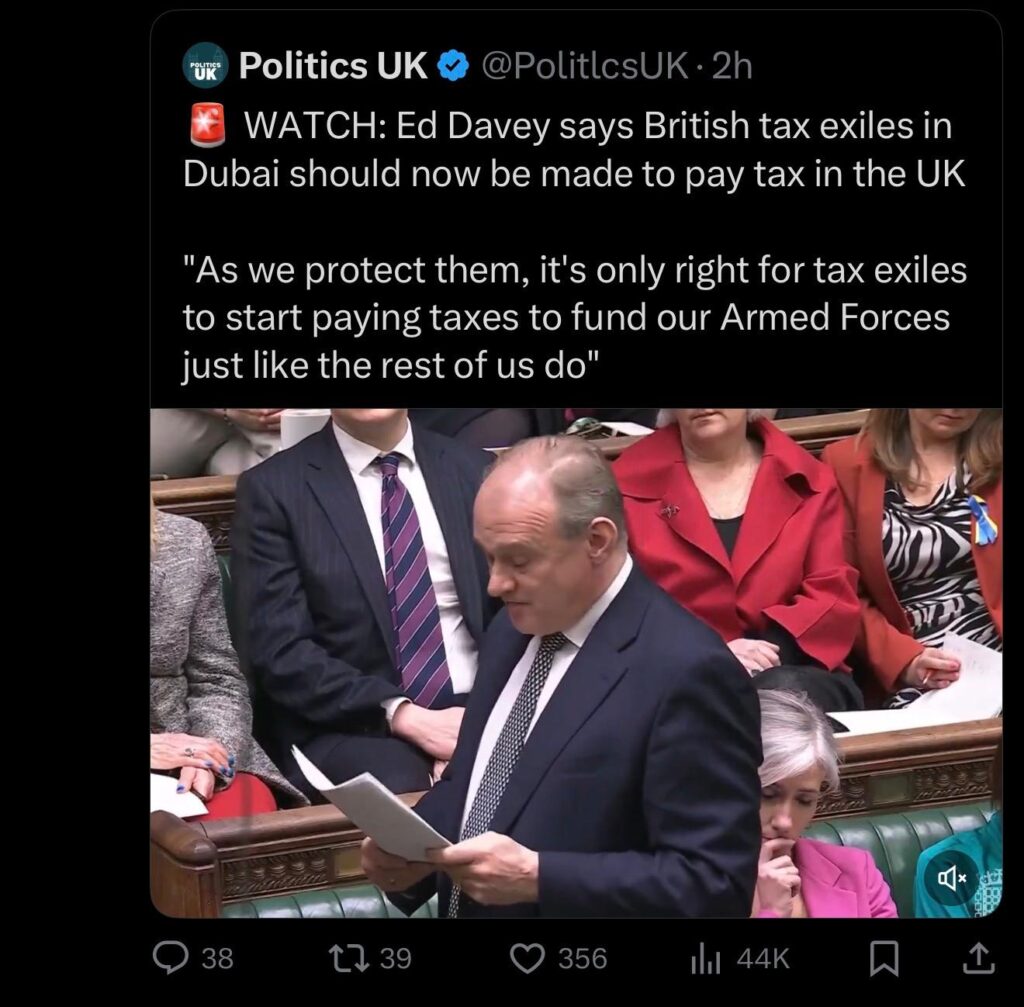

As the UK government plans support options for British nationals caught up in escalating regional tensions in the Gulf, Liberal Democrat leader Sir Ed Davey has argued that British “tax exiles” in Dubai should be made to pay UK tax because “we protect them” and that it is “only right” they contribute to fund the Armed Forces.

It is the kind of UK political line we have sadly become used to. Clippings for social media.

But in reality, this contribution is about as substantial as the content of those ‘Dubai influencers’ he and his ilk seem to malign so much.

Consular support is not a reward for paying UK tax.

Tax residence is not a loyalty points card for citizenship.

And the much cited “100,000+ registered Britons” figure is not an evacuation queue.

These aren’t quite the last days of Saigon.

Let’s attempt to look at the law.

WHAT “CONSULAR ASSISTANCE” IS (AND WHAT IT ISN’T)

Overview

The Foreign, Commonwealth and Development Office (“FCDO”) defines[1] consular assistance as the support UK embassies, high commissions and consulates can provide to British nationals who get into difficulty while living or travelling abroad.

This includes lost passports, hospitalisation, arrest/detention, victims of crime, deaths overseas, and so on.

The key words are support and can. The same FCDO guidance is explicit that:

This matters because the public debate often treats “consular support” as if it were a contractual entitlement. In other words, “I paid in, therefore you must extract me” and, of course, the opposing view that you don’t get any support as you’ve had the temerity to go and work abroad.

But that is not how it works.

Consular assistance is a function of nationality and state capacity. It is carried out through diplomatic / consular networks, constrained by local law and politics, and (in UK law) largely exercised as a matter of policy and discretion.

It is not enforceable personal right.

The connecting factor is nationality, not tax residence

If you want the cleanest, most direct statement for your article, it is sitting in black and white on GOV.UK[2]:

“As a British national, you can receive our assistance even if you do not normally live in the UK.”

That sentence is doing a lot of work. It severs the lazy assumption that “living abroad” (and the tax consequences that may follow) downgrades someone’s relationship with the state.

The FCDO’s eligibility test is essentially: “are you a British national (or otherwise within a defined crisis-related exception)?

It’s not… “are you UK tax resident?”

It’s not… “have you paid UK income tax this year?”

It’s not… “do you pay more into the Treasury in taxes than you take out in welfare and benefits?”

It’s not… “do you pass the moral purity test of a radio phone‑in?”

Where does consular assistance “come from” in law?

The answer has three layers:

International law framework: the Vienna Convention on Consular Relations (1963)

The Vienna Convention on Consular Relations 1963 (VCCR) is the key treaty setting out what consular posts do and how they operate.

Two provisions are especially relevant.

Firstly, Article 5 lists “consular functions,” including protecting the interests of the sending state and its nationals in the receiving state (within international law limits).

This is not a “taxpayer service”. It is a classic incident of statehood. In other words, states look after nationals abroad, as far as they can, consistent with the host state’s sovereignty and local law.

Secondly, Article 36 VCCR confers specific rights in detention cases: the detainee must be informed of the right to consular notification, and consular officers must be permitted to communicate with and visit the detained national (subject to local procedures).

Domestic UK law: giving effect to the Convention (and what it does not do)

The UK gives effect to the VCCR through the Consular Relations Act 1968[3].

But here is the important point – incorporation does not equal a domestic enforceable entitlement to “help me”.

A parliamentary evidence paper summarised it plainly:

This is why the “where is it in UK statute?” question often leads to confusion.

The UK’s consular system is not built as a statutory welfare entitlement. It is built as an executive function.

Domestic Constitutional Power

In UK constitutional law, foreign affairs (including consular action) sits largely within executive power, historically the royal prerogative, exercised through ministers.

The Supreme Court’s decision in R (Sandiford) v Secretary of State for Foreign and Commonwealth Affairs [2014] UKSC 44 is unusually useful here because it puts the architecture on the record:

Summary

UK consular assistance is a prerogative / policy function. It is not (generally) a statutory duty owed to an individual. A parliamentary evidence submission (drawing on UK litigation) goes further:

“British nationals do not have a legal right to consular assistance overseas…

The UK Government is under no general obligation under domestic or international law to provide consular assistance … [it] is exercised on the basis of administrative discretion.”[6]

WHY IT DIFFERS FROM TAX RESIDENCE (AND WHY THAT DIFFERENCE IS THE POINT)

Overview

The reason this debate goes wrong is that it drags a tax concept into a nationality/foreign affairs context.

UK tax is (almost entirely[7]) residence‑based

In the UK, residence status affects whether you pay UK tax on foreign income (and, exceptionally, some UK income[8]).

The GOV.UK[9] page summarises the broad principle for the non-tax reader:

Additionally, the same can be said for capital gains tax and also, more recently, for Inheritance Tax (“IHT”) that was previously primarily determined by one’s domicile.

The mechanism for deciding residence is the Statutory Residence Test, introduced in Finance Act 2013, Schedule 45.

So, yes, residence is generally the connecting factor for UK tax.

That is a deliberate policy choice.

It is also internationally normal.

Citizenship‑based taxation is the outlier (US and…err… Eritrea)

If the political suggestion is “if you have a British passport, you should pay British tax wherever you live”, then you are asking for the UK to move toward a citizenship‑based model.

The United States is the canonical example. If you are a U.S. citizen living abroad, the IRS is still very much interested in you as your worldwide income remains subject to U.S. income tax regardless of where you live (subject to exclusions/credits)[10].

Eritrea is often cited because of its “diaspora tax”; the UN Security Council has condemned Eritrea’s use of a “Diaspora tax” in the context of regional destabilisation and sanctions issues.[11]

Whether one admires or dislikes those systems, the point is simple. Linking consular help to UK income tax implies a fundamental redesign of the UK’s tax basis from residence to citizenship.

That is not a small fairness tweak. It is a structural shift with sprawling consequences:

If someone wants that debate, fine. Have it.

But have it honestly, with the label on the tin.

WHAT ABOUT THE HOST COUNTRY?

Of course, the likes of Davey also ignore the fact that the ‘exile’ is living in another country.

The economy and state of the UAE is very different to the UK.

First of all, there is a genuine economy. We are not talking about an island of brass-plates in the middle of the sea. From Finance to tourism, law to education, AI to transport.

Secondly, the state is very different. You pay for education, health and pretty much everything else.

You pay corporation tax, VAT and also, if you are in business, annually for trade licences etc. This, along with taxes on natural resources, funds the state.

You can argue as to the rights and wrongs of that. But that’s the way it is.

So, what is this premise that ‘we protect them?’

Was it the Royal Air Force shooting down missiles over Dubai and Abu Dhabi at the weekend. Well, not that I can see. [At the time of writing, reports were 2 x drones heading for Cyprus and 1 x drone heading for Qatar. Happy to correct if I am wrong]

I confess, I did not know a great deal about the UAE’s air defence system until the weekend:

Developed by Lockheed Martin, THAAD is designed to intercept ballistic missiles during the final phase of their flight…

… The UAE became the first country outside the US to deploy THAAD, acquiring the system as part of a multibillion-dollar defence agreement.”[12]

This is a system paid for by the UAE state… not Ed Davey or the British state.

This is also a system that protected the locals, the ‘exiles’, the other immigrants that have moved to Dubai, the stranded holidaymakers and those who simply found themselves in transit.

THE 102,000 FIGURE: WHAT IT IS… AND WHAT IT IS NOT

This is where the rhetoric gets especially slippery.

Reuters reports[13] that UK ministers estimate around 300,000 British citizens are in Gulf countries (including residents, holidaying families, and some in transit), and that 102,000 people in the region have registered their presence with the UK government since attacks began.

That number has been framed in commentary as if it is:

But the UK government’s own phrasing is different.

On 1 March 2026, the FCDO published a news story urging British nationals in specified countries to register their presence “to receive direct updates” from the FCDO[14].

And the UAE travel advice page states plainly that registering your presence is “for further updates.”[15]

So, the accurate characterisation is:

Registration is a mailing list for information, not a waiting list for evacuation.

CONCLUSION

Sir Ed Davey’s LBC interview contains an important concession that undercuts the posture. He says, in substance, ‘we absolutely owe a duty to them. They are British.’[17]

That sentence is closer to the real constitutional spirit. And, although it may be considered a duty, not an individual right as explained above

But then he pivots to ‘they should be made to pay UK tax because they benefit from protection.’

This is where the opportunism creeps in. Because it bundles together three different ideas:

…and pretends they are on the same moral ledger.

As I hope I have explained, they are not.

It’s disappointing, but hardly surprising, to see a politician stand up in Parliament and talk like this.

Of course, in this era of vibe politics, it is perhaps not a surprise that a politician cannot resist an opportunity clamber on to a soap box, to say “tax dodgers” a few times, and fill up their social-media channels.

[1] https://www.gov.uk/guidance/consular-assistance-how-the-foreign-commonwealth-development-office-provides-support

[2] https://www.gov.uk/guidance/who-the-fcdo-can-support-abroad

[3] https://www.legislation.gov.uk/ukpga/1968/18

[4] https://committees.parliament.uk/writtenevidence/48163/html/

[5] https://supremecourt.uk/uploads/uksc_2013_0170_press_summary_5f2edcd97b.pdf

[6] https://committees.parliament.uk/writtenevidence/48163/html/

[7] With domicile removed almost exclusively from UK statutute books, I can only think of domicile still being relevant under double tax treaties (where residence is, of course, primarily an issue too. But its early in the morning…)

[8] For example, a non-Uk resident will not pay UK income tax on UK dividends (though there is anti-avoidance machinery around that too

[9] https://www.gov.uk/tax-foreign-income/residence

[10] https://www.irs.gov/individuals/international-taxpayers/frequently-asked-questions-about-international-individual-tax-matters

[11] https://docs.un.org/en/S/RES/2023%282011%29

[12] https://www.wired.me/story/inside-the-system-that-intercepted-missiles-over-the-uae-today

[13] https://www.reuters.com/world/uk-sending-rapid-teams-help-citizens-leave-middle-east-2026-03-02/

[14] https://www.gov.uk/government/news/foreign-office-travel-advice-updates

[15] https://www.gov.uk/foreign-travel-advice/united-arab-emirates

[16] https://www.thetimes.com/uk/transport/article/evacuation-dubai-news-iran-war-g9k0rnw6x

[17] https://www.lbc.co.uk/article/tax-exiles-dubai-pay-britain-ed-davey-5HjdTkL_2/