ANDY BURNHAM & LAND VALUE TAX: THE “LEAST BAD TAX” THAT BRITAIN KEEPS FLIRTING WITH

Read more

June 19, 2026 | 9 min read

Author: Andy Wood

Intro

In 1974, Sparks released their gloriously unhinged hit “This Town Ain’t Big Enough for Both of Us.”

Fifty-two years later, we have two very different political acts, Wes Streeting and the Green Party, fighting over the same peculiar tune of aligning CGT with income tax.

The message is from both… ‘This tax ain’t big enough for the both of us!

That tax, of course, being CGT.

With a Burnham-led administration seemingly a matter of ‘when not if’ it still remains whether Streeting will be an important part of that administration going forward, or whether he has simply been a useful idiot.

In case it is the former, let’s have a detailed look at the sheet music and examine both acts’ chops

Bass line

Streeting’s Proposal, announced 21 May 2026, was as follows:

On the other hand, this has been the policy of the Green Party for a while and was in their 2024 manifesto or, as I call it, the Badger Budget:

Further, Zack Polanski reiterated in November 2025 that “income from work should not be taxed more than income from wealth”

Welcome to the Badger Parade

Almost a song by My Chemical Romance, but very much my take on the Green’s 2024 election manifesto.

The Greens’ income tax and NIC proposals were, I conceded, a fairly sensible idea.

However, it was the wealth, IHT and capital gains section where, I wrote, “to channel Harry Hill, begins the badger parade.”

The CGT alignment sat squarely in the middle of said parade.

Fast forward to 2026, and the former Health Secretary has dusted off the same policy and is selling it as the centrepiece of his leadership pitch.

The badger has moved from being an alternative act to the mainstream.

The fundamental difference is perhaps that Streeting sets out his stall as a “wealth tax that works” whereas the Greens would have it alongside a wealth tax.

Problems with aligning CGT and income tax

Overview

The case for alignment is perhaps intuitive with a ‘pound being a pound’.

But is a pound really a pound?

Tax policy has spent the best part of the last century wrestling with precisely that question.

A pound earned from a 60-hour working week feels different to a pound arising from the sale of a family business built over thirty years.

That feels different again to a pound generated by a buy-to-let portfolio.

Different again to a gain on a painting that sat on a wall appreciating quietly for two decades.

The moment we acknowledge those differences and want to do something about them, complexity knocks at the door.

Simplicity and fairness are often presented as partners. In reality they are frequently fearsome foes.

The simplest tax system would apply the same rate to everything.

The problem is that most people immediately start identifying situations where that would feel unfair.

And that, Ladies and Gentlemen, is how tax legislation acquires its thousands of pages.

Inflation punishment

Unlike income, capital gains accrue over years, sometimes decades.

A gain of £100,000 on an asset held for 20 years includes a substantial element of pure inflation.

Tax that at 45% and you’re taxing phantom gains.

We have spent decades oscillating between treating capital gains as something fundamentally different from income and treating them as essentially the same thing.

Sometimes we align the rates. Sometimes we separate them.

Sometimes we compensate for inflation through indexation. Sometimes through lower rates. Sometimes through neither

The history of CGT is, in many respects, the history of governments repeatedly changing their minds about what exactly a capital gain is

Streeting, to his credit, addresses the issue of inflationary profits directly. He proposes “new allowances for reinvestment, entrepreneurs and indexation, so that inflationary gains aren’t taxed at all.”

On the other hand, the Greens’ manifesto was silent on the point.

Bunching

Gains often crystallise in a single year, the sale of a business, a property, a share portfolio. Push that into income tax bands and a lifetime’s accumulation gets taxed at the top marginal rate.

Is this fair?

Arguably, not.

Some form of top-slicing relief (as exists for life insurance chargeable events) might be the fairest route to avoid cliff-edge outcomes.

Lock-in effect

Higher CGT rates encourage asset owners to hold rather than sell, the classic “lock-in” problem.

This reduces market liquidity, distorts investment decisions, and paradoxically may reduce revenue as fewer disposals occur.

Business assets

Should a founder selling their company face the same rate as someone cashing in a second home?

Business Asset Disposal Relief exists precisely because we want to encourage entrepreneurship.

Streeting nods to this with “carve-outs for genuine entrepreneurs taking risks building companies”, but defining “genuine” is where policy gets messy.

Death and the double-tap

Currently, assets receive a CGT-free uplift on death (the heir inherits at market value).

If CGT rates match income tax, pressure grows to either (a) tax gains at death, or (b) remove the uplift or the lock in effect (and to death) described above becomes very real.

Either change would be seismic for estate planning and family businesses.

The residence question

Main residences remain exempt from CGT.

That exemption has become so embedded in British political culture that most people barely notice it exists.

Yet it represents one of the largest and most valuable tax reliefs in the system.

If the argument is that “a pound is a pound”, why should a gain on a family home be exempt whilst a gain on shares, a business, or an investment property is taxed?

The answer is political rather than economic. We have collectively decided that some gains are “good gains” and some are not.

Of course, taxing main residences would be political suicide.

—

None of these objections is fatal.

But they explain why CGT alignment, for all its intellectual appeal, has remained perpetually on the “too hard” pile.

And why a ‘pound is a pound’ is not quite so easy as one might think!

Does raising CGT rates naturally increase revenue?

Both acts are promising £12bn from this policy.

The Centre for Analysis of Taxation estimated £14bn in 2024. But these figures assume taxpayers behave like sheep rather than cunning weasels and, well, unpredictable badgers.

As I noted back in 2024 “When in danger of a serious loss to their plumage, the wealthy do something about it.”

This might be to defer the sale of assets.

It might be to decamp to a different jurisdiction, subject to how this fits into their personal and business objectives (hey, tax isn’t the most important thing in the world!)

Anticipating, and blocking such obvious behavioural responses, are not beyond the wit of man or woman, of course.

But is the £12bn figure a realistic one in any event?

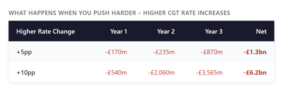

The Government publishes a “ready reckoner” showing estimated revenue effects of illustrative tax changes. The June 2025 edition, crucially, after Reeves’s October 2024 increases to 18%/24%, tells a striking story.

What happens if you increase CGT rates by just one percentage point from current levels?

The lower rate increase nets about £10m across three years. That’s a rounding error.

The higher rate increase? Net +£35m… but negative in two of the three years. Again, essentially background noise.

This is the revenue effect of a single percentage point increase. Streeting wants to go from 24% to 40% or 45%, which is a 16-21 percentage point jump.

Note 14 of the bulletin explains the dynamic:

“Very large tax rate rises can reduce exchequer yield due to taxpayer behavioural impacts.”

But you don’t need “very large” rises to hit the wall. The 2025 data shows that even marginal increases from current rates produce negligible or negative returns. The Reeves Budget appears to have taken us to — or past — the revenue-maximising point.

The larger illustrative increases confirm this:

Larger rises = larges LOSSES to the Treasury

As such, in the absence of any other action not contemplated in the Government figures above, the Green’s and Streeting’s proposal would likely lose billions.

Conclusion

This tax… and I mean CGT… ain’t big enough for both of them.

Streeting and the Greens are now competing for ownership of the same CGT alignment policy, both promising the same £12bn, both convinced they’re the authentic article.

The difference?

When the Greens proposed it, it was one item on a long menu of redistributive measures, CGT alignment sat alongside a wealth tax, higher income tax bands, and a gaggle of other “tax the rich” policies.

It was part of what I called the Badger Parade. A manifesto that can only be described as the cynical plucking of Colbert’s goose, playing to the party’s tax-the-wealthy support base.

Streeting’s pitch is fundamentally different in positioning, if not substance.

His CGT proposal is the centrepiece of a “progressive capitalism” agenda – a standalone reform designed to signal pro-growth, pro-fairness credentials.

In his more recent FT essay, he frames it explicitly as being about making markets work better, not about soaking the rich. “The balance needs to be tipped from work to wealth,” he writes, but crucially adds that “half of capital gains taxpayers would be better off” under his proposals.

The Greens want to tax wealth because they think the wealthy have too much. Streeting seemingly wants to position any tax on wealth as a solution to the fact we’re taxing labour too much.

As Sparks might say, this tax may not be big enough for the both of them.

The difficulty is that every attempt to simplify tax eventually creates a fresh source of Angst in Our Pants.